Launch of branded product into mental health market

The Challenge

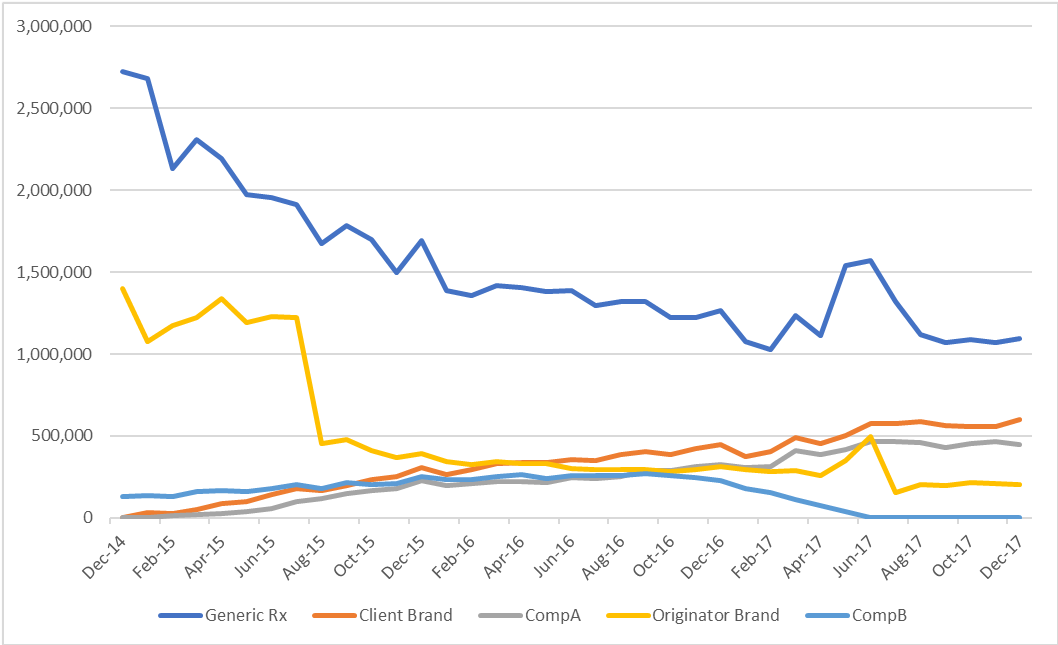

Launch of a branded prolonged release antipsychotic drug into the market

Many generic scripts in the market written generically and the perception that generic prescribing was the lowest cost option

Many CCG’s saw the best cost saving scheme was to move from MR preparations to IR preparations

Push back from pharmacists and dispensing doctors who would loose profit by moving to branded generic

Moving away from generic prescribing meant that had to be confidence in supply chain as the brand would have to be readily available

Many competitors introduced into the market at the same time.

Our Approach

Target CCGs with cost and patient benefit message

In-house data sources allows bespoke CCG materials.

Specialist savings information, supply chain and pricing information.

Provision of review service to support prescribing changes.

Data systems changed to reflect product of choice

Implementation of Dispensing Doctor schemes.

Timed localised wholesale and retail campaign in CCGs where on formulary

Targeted rebates as required

Results

Dominant market share gained within 18 months, taking product to brand leader position.

Gaining 121 CCG formulary inclusions.

Exceeded client growth expectations by 21%.

• Brand leader within 18 months

• Brand originator price reduction did not slow growth

• Competitors failed to match growth even with better price offer

Launch of preservative free eye drop range

The Challenge

To launch a range of preservative free eye drops in a multi dose dropper bottles to the primary care market

Competing with less expensive preserved drops

Preservative free historically meant unit dose vials- patient education

Primary care did not initiate treatment or make switches without secondary care endorsement

Our Approach

To target major secondary care eye units and engage in peer to peer discussions to gain endorsements, regarding patient and environmental benefits

Gaining hospital formularies and utilizing this endorsement at primary care level. Utilizing advocates in one region to influence others

Establishing a need for preservative free product in a multi dose bottle Vs UDV’s

Development of materials for patients on use of dropper bottles to aid compliance and acceptance of the delivery device

Tele-marketing campaign to all CCGs

Pull through by patient reviews and PCN pharmacist involvement

Sponsorship of society meetings to gain contacts and create awareness of the brand

Results

Defining the company previously not know in the ophthalmology field as a major player in this arena

Gaining all key eye hospital formularies. and endorsement

Gaining 201 CCG formulary inclusions

Gaining 51% market share

Over 50% market share after 21 months in the market

Key eye centres ordering directly after 12 months in the market

Stroke review service for pharma client

The Challenge

Launch Product in a therapy area where there were already 3 other leading competitor brands

Large Pharma companies had already secured a stronghold

Obtaining both secondary and primary care formulary inclusion

Establishing first line positioning

Develop a robust mechanism for PCO’s to change from the ‘big 3’ brands to the client’s product

Covid 19 – issues with access to primary care sites

NHS need to move patients from Warfarin to a DOAC

How to become this DOAC of choice

Our Approach

Target CCGs with cost and patient benefit message

Interventions to reduce incident of ischaemic stroke

Optimise dose and treatment plans

Enhance patient monitoring and reduce adverse effects

Bespoke CCG materials from inhouse data

Both onsite and remote access available

Data systems changed to reflect product of choice

Results

Results to date – service is still active

Product of choice in reviewed CCG’s

400% growth in reviewed CCG’s (Qtr vs Qtr)

Moved from 4th to 2nd place market position in reviewed CCGs – Rx Volume

Effect of Rx review in Completed CCG’s

Rx value

Effect of Rx review in individual CCG’s Rx Value